We’re back! This week, we have dedicated the post to providing a summary of the proposed tax changes in Governor Cuomo’s Executive Budget for fiscal year 2022. We’ve already covered some of the proposed tax changes in the Executive Budget that came out late last month (see here, here, and here). The Budget Proposal sets forth new taxes, credits, and other initiatives, aimed largely at mitigating the revenue shortfalls caused by the COVID-19 pandemic, and are broken down into the following categories:

- Responding to COVID-19;

- Tax Cuts and Credits;

- Reform and Simplification;

- Enforcement and Compliance Initiatives;

- Other Actions;

- School Tax Relief (“STAR”) Program Actions;

- Gaming Initiatives; and

- Fee Actions

While the Executive Budget contains a variety of important provisions, we will spend this week discussing noteworthy proposals under the following categories: Responding to COVID-19, Enforcement and Compliance Initiatives, and Other Actions which are found in either the Revenue Bill (“REV”) or the Transportation, Economic Development, and Environmental Conservation Bill (“TED”), as indicated below. Two of the more interesting proposals include allowing the Department of Taxation and Finance the ability to appeal Tax Appeals Tribunal decisions and the proposed pass-through entity workaround to the limitation on federal state and local tax deductions. Next week, we’ll dive into the remaining initiatives in the Executive Budget before returning back to our weekly legislative updates.

- Responding to COVID-19:

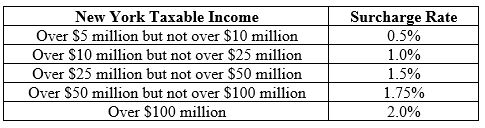

a. Enact Temporary PIT High Income Surcharge (REV Part A)

As expected, the Executive Budget proposes higher personal income tax rates for taxpayers with taxable income over $5 million per year. Styled as a “surcharge,” this tax increase would go into effect for tax years 2021-2023. The proposal estimates this surcharge will generate approximately $1.5 billion in fiscal 2022 alone. The surcharge will be based on New York taxable income and the following bracket rates apply:

We discussed the implications for taxpayers who pre-pay estimates. At a basic level, the pre-payers get their pre-payments returned to them as credits against surcharges in 2022 and 2023, and then again in the form of grossed-up deductions against the regular tax applied against them in 2024 and subsequent years. Though we suggest waiting until further guidance becomes available before making these pre-payments.

b. Delay Middle Class Tax Cut by One Year (REV Part B)

The Executive Budget would pause the phase-in of the middle-class tax cut, which began in 2018 and was scheduled to fully phase in by 2025. The tax rates for 2020 will remain in effect for another year. Going forward, the tax rates will be bumped back one year. For example, the tax rates planned for 2021 will take place in 2022, the tax rates planned for 2022 will take place in 2023, and so on and so forth.

c. Enact the Pandemic Recovery and Restart Program (TED Part TT)

The Executive Budget would establish the Pandemic Recovery and Restart Program which would add three new tax credits specifically intended to provide relief for small businesses in certain industries—specifically those in the accommodation, arts and entertainment, restaurants, and musical and theatrical production industries—to recover for the pandemic. The three new credits would be as follows:

- Small Business Return-to-Work Tax Credit: This refundable tax credit would be available to small businesses that have experienced year-to-year revenue or job losses of at least 40% in qualifying industries. Small businesses that hire additional workers will be eligible for a tax credit of $5,000 for each net full-time position added, with a maximum credit of $50,000 per business. The amount of total credits available under this program would be capped at $50 million and would be administered by the Department of Economic Development (“DED”).

- Restaurant Return-to-Work Tax Credit: This refundable tax credit would be available to small, independently-owned restaurants that: (i) are located within New York City that were subject to a ban on indoor dining for over six months, or (ii) restaurants outside of New York City in areas that were designated as a red or orange zone for at least 30 days. Similar to the credit discussed above, this credit would only be available to those restaurants that have experienced year-to-year revenue or job losses of at least 40%. Restaurants that hire additional workers will be eligible for a tax credit of $5,000 for each net full-time equivalent position added, with a maximum of $50,000 credit of per business. The amount of total credits available under this program would be capped at $50 million and would be administered by DED.

- NYC Musical and Theatrical Production Tax Credit: This program would be available to qualified musical and theatrical production companies, and would provide a refundable tax credit equal to 25% of the sum of its production expenditures incurred by December 31, 2021, with a maximum of $500,000 per production company. The term “qualified musical and theatrical company” means a business that produces a musical or theater production in New York City and spends at least $1 million dollars in qualified production expenditures. The amount of total credits available under this program would be capped at $25 million and would be administered by DED.

d. Enact Employer Child Care Credits (REV Part D)

The Executive Budget would create the Excelsior Child Care Services Tax Credit, whereby participants in the Excelsior Jobs Program would receive a 6% Excelsior Child Care Services Tax Credit for ongoing net child care expenditures provided by the participant. Additionally, the Executive Budget would expand the Excelsior Investment Tax Credit from 2% to 5% for the provision of child care. Furthermore, the proposal would enhance the existing Employer Provided Child Care Credit by doubling the current credit percentages to 50% of qualified child care expenditures and 20% of qualified child care resource and referral expenditures. The proposal would also increase the “per entity cap” from $150,000 to $500,000.

- Enforcement and Compliance Initiatives:

a. Enact an Elective Pass-Through-Entity Tax (REV Part C)

The Executive Budget would create a new Article 24-A of the Tax Law, to provide an elective pass-through entity (“PTE”) tax beginning January 1, 2022. The workaround is designed to mitigate the impact of the $10,000 cap on state and local tax (SALT) deductions enacted in the Tax Cuts and Jobs Act (“TCJA”). The election would only be available to partnerships and S corporations that are comprised solely of individual partners or shareholders. If the entity validly elects into the PTE workaround, it would be required to pay tax at a rate of 6.85% on its partnership taxable income or S corporation taxable income (as defined by the legislation).

We discussed how many states have enacted similar workarounds permitting partnerships and S corporations to pay tax at the entity level in order to combat the negative impacts of the (highly politicized) SALT cap. The theory behind these workarounds is that, because the SALT cap applies only to individuals, state and local income taxes applied at the entity level should be fully deductible at the Federal level without regard to the individual limitation. Especially given recent IRS approval of PTE workarounds, it was only a matter of time before New York enacted similar legislation.

The Executive Budget would also amend Tax Law § 606 to add a PTE tax credit and would further amend Tax Law § 620 with respect to the existing resident credit. Resident credits are a crucial facet of any PTE workaround regime.

b. Increase Wage and Withholding Filing Penalty (REV Part G)

The Executive Budget would increase the maximum penalty for employers who fail to timely and accurately file wage and withholding reports. Currently, such fines are $50 per employee per report, capped at $10,000. The proposal would increase the penalty from $50 to $100 per employee, and increase the maximum from $10,000 to $50,000 to “incentivize reporting accuracy.”

However, this will likely be problematic for employers who are already struggling with how to properly withhold on nonresident employees working remotely due to COVID-19. States are all over the map on this issue. Many were hoping that New York would allow the “bona fide employer office” safe harbor to be used to alleviate some of the potential problems that could be created by telecommuting employees. However, New York made its position clear in a Residency FAQ updated last October: nonresident employees working remotely due to COVID-19 are still to be considered days worked in New York unless the employer has established a bona fide office at the telecommuting location. However, New Hampshire announced a lawsuit against Massachusetts, seeking to enjoin the Commonwealth from enforcing its new telecommuting regulation against New Hampshire residents that may be taken up by the Supreme Court, which could potentially change the legality of New York’s position. So stay tuned!

In addition to the proposals described above, the Budget Proposal also plans to update tax preparer regulation and enforcement, enhance real estate transfer tax compliance, and increase interest free period for certain sales tax refunds.

- Other Actions:

a. Enact the Cannabis Regulation and Taxation Act (REV Part H)

For the third consecutive year, the Executive Budget proposes legalizing and taxing adult-use cannabis. The proposal would create a new Article 20-C of the Tax Law which would create two new taxes to be imposed on the adult-use of cannabis:

- A wholesale THC-based tax at various rates according to the potency level or THC content of different product categories. For example, edibles would be taxed at a rate of $0.04 per milligram of THC, concentrates would be taxed at $0.01 per of milligram total THC, and cannabis flower would be taxed at rate of $0.007 per milligram THC. This whole THC-per-milligram tax would be imposed on the transaction that occurs on the sale from the wholesaler to a retail dispensary;

- A surcharge of 10.25% of the retail sale price will apply to the sale of adult-use cannabis products by a retail dispensary to a consumer;

Additionally, sales and use tax would be imposed on the retail sale by a dispensary to a consumer.

The Executive Budget’s regulatory framework would be administered by the newly established Office of Cannabis Management (“OCM”). The OCM would also be responsible for the licensing, production, distribution, and enforcement of cannabis products in the adult-use, industrial, and medical cannabis markets. For more details on this section of the Executive Budget, and for continued updates on the Hemp and Cannabis industry, please refer to our Hemp and Medical Cannabis experts here.

b. Allow DTF the Right to Appeal DTA Tribunal Decisions (REV Part T)

The Executive Budget would allow the Department of Taxation and Finance (“DTF”) the right appeal the decisions of the Tax Appeals Tribunal. Currently, only a taxpayer has the right to appeal an adverse decision of the Tax Appeals Tribunal. This provision of the Budget would allow the DTF the right to seek judicial review of an adverse decision.

This proposal is similar to failed proposal from 2019. While the Memorandum in Support of the proposal claims that the DTF’s inability to appeal Tribunal decisions is a “flaw” in current law, our view is that a change like this would substantially increase litigation burdens on New York taxpayers. And since the Tribunal is technically already part of the DTF, it seems odd to give the DTF the right to appeal decisions coming from its own agency!