We’re back to our regularly scheduled programming. For the last two weeks, we took a break from tracking legislative developments to provide a summary of the proposed tax changes in Governor Cuomo’s Executive Budget for fiscal year 2022. In addition to our overall summary of the Executive Budget, we also took an in-depth look at some of the more noteworthy changes. (See here, here, and here.)

As discussed in our last update, we continue to see bills reintroduced that expired at the end of the last session. Two of the more interesting proposals include imposing a surcharge on certain taxpayer’s investment income and an excise tax on sugary drinks.

- A.B. 2526 – Tax Credit for Parents Home Schooling Their Children

This bill, a reintroduction of A.B. 6676A from last session, would provide a refundable personal income tax credit for parents who are home schooling their children equal to the cost of “learning materials” purchased for home school purposes during the taxable year. “Learning materials” is broadly defined to include items such as textbooks, workbooks, supplemental reading materials, videos and software. The credit is capped at $2,400.

- A.B. 3152 – Investment Income Surcharge

Effective January 1, 2022, this bill would amend Tax Law § 612 to impose a surcharge on taxpayers in an amount equal to the disparity between federal tax rates that apply to income derived from labor and from capital gains. The surcharge would be imposed on the share of a taxpayer’s New York taxable income that is taxed at the federal capital gain rate in an amount equal to the difference between the federal ordinary income tax rate and the federal capital gain tax rate for such individual.

The “surcharge” proposed in this bill represents another example of the state looking to new taxes on individuals as a way to mitigate the budget deficit. The justification confirms this by stating the intent of the bill to provide needed revenue through the taxation of investment income from high earners.

- S.B. 2522 – Tax on Low-Taxed Investment Income

This bill would amend the Tax Law to add § 601-b that would impose an additional tax on “low-taxed investment income.” The text explains that low-taxed investment income is the amount of a person’s New York State taxable income attributable to long-term capital gain, dividends, or other income taxed under the preferential rates of IRC § 1(h). To calculate the additional tax, a taxpayer would take the difference between the applicable federal ordinary income tax rate and the applicable federal tax rate imposed at the rates under IRC § 1(h). However, this additional tax would only apply to taxpayers whose income meets or exceeds certain threshold based on filing status, specifically: $150,000 for single filers, $200,000 for head of household, and $250,000 for joint filers.

Similar to the proposal described immediately above, this bill is another example of the state looking to new taxes on high earners as a way to mitigate the budget deficit being faced due to COVID-19.

- S.B. 2566B – “Save Our New York State Restaurants Act”

This bill, a reintroduction of S.B. 9050 from last session, would authorize a sales tax exemption for sales of food and drinks at restaurants and taverns during a specific one-month period, and would allow municipalities to grant the same exemption.

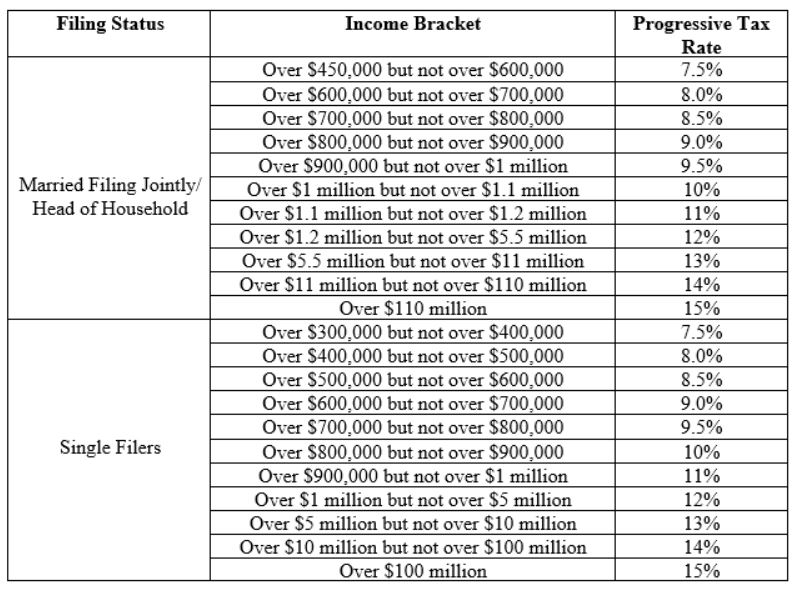

- S.B. 2622 – Progressive Income Tax for High Earners

This bill proposes amending Tax Law § 601 to raise the tax rates for taxpayers in the upper brackets by establishing what the bill describes as “imposing a progressive income tax structure” effective immediately.

This bill is the latest in a line of recently introduced bills this legislative session that would extend the state’s income tax rates. (See also S.B. 917, S.B. 1194, and S.B. 1513). This bill is another example of the state looking to new taxes on individuals as a way to mitigate the budget deficit

- S.B. 4528 – Tax on Corporate Buybacks of Issued Shares

This bill, a reintroduction of S.B. 7629 from last session, would impose a tax of 0.50% on all corporate stock buybacks of issued shares. Under current law, there is a tax imposed on the purchase, redemption, or other acquisition by a corporation of its stock, unless such shares are cancelled pursuant to Business Corporate Law § 515. This bill would impose a tax on the reacquisition of stock by a corporation even if such corporation subsequently cancels such stock.

This newly-imposed tax is another example of lawmakers looking to new taxes on businesses as a way to mitigate the budget deficit.

- S.B. 4602 – Excise Tax on Sugary Drinks

This bill would establish a tax on beverages with high levels of sugar. The nutrition facts label will be used to determine the amount of sugars per twelve ounces of drink. Manufacturers, bottlers, wholesalers, or distributors will be required to add the taxes imposed by this bill to the retail price of the sugary beverage.

Certain beverages would be exempt from the sugary drink excise tax, including beverages with 100% natural fruit or vegetable juice with no added sugar, milk and milk substitutes, infant formula, coffee or tea without added sugars, beverages for medical use, etc.

Similar proposals have been introduced in Hawaii and Massachusetts, and a number of cities have already adopted an excise tax on sugar-sweetened drinks. As we have seen throughout this legislative session, the State is increasingly looking to new and alternate forms of revenue in order to compensate for the revenue shortfalls due to COVID-19.