New Tribunal Case Offers Up a New Framework for Answering this Question

New York’s two-part test for statutory residency has been heavily litigated over the years, and one of the biggest issues has involved the determination as to whether a taxpayer maintained a “permanent place of abode.” In 2014, the State’s highest court in Gaied v. NYS Tax Appeals Tribunal struck down the Tax Department’s overly-broad interpretation of “permanent place of abode” in favor of a more sensible interpretation. In doing so, the High Court declared that in order for a place to constitute a permanent place of abode (“PPA”), “there must be some basis to conclude that the dwelling was utilized as the taxpayer’s residence.” And later in the decision, the Court opined that to qualify as a PPA, “the taxpayer must, himself, have a residential interest in the property”

But that 2014 ruling has only engendered more confusion. In the aftermath of Gaied, everyone started fighting about what constitutes a “residential interest” in a dwelling. And at the heart of this dispute was the question of whether the taxpayer must personally use the dwelling as a residence in order for it to be a PPA. To us, the answer seemed obvious, since the Gaied Court specifically held that the dwelling “must be utilized as the taxpayer’s residence.” But alas, disagreements remained. The Tax Department issued new audit guidelines [click HERE for guidelines, see page 54 at Example 1], and took the position that usage wasn’t necessarily required. Under the Department’s view, if a taxpayer had a property right in a dwelling and no one else used it, that was enough to make it a PPA.

Well, it took a while, but the New York’s Tax Appeals Tribunal has finally weighed in on the PPA test, in Matter of Mays, the first substantive decision on the PPA issue by the Tribunal since Gaied. And though the actual issue in that case wasn’t all that interesting (the taxpayer argued that a temporary corporate apartment that she used exclusively was not a PPA), the Tribunal took the time to walk through the legal issue in a step-by-step, comprehensive manner, synthesizing a number of different rulings to set the framework for analyzing the PPA issue. Funny though, because the actual holding wasn’t that controversial, the case received little fanfare in New York residency circles. Our favorite blogger picked it up, but so far no one seems to be talking about. So we will!

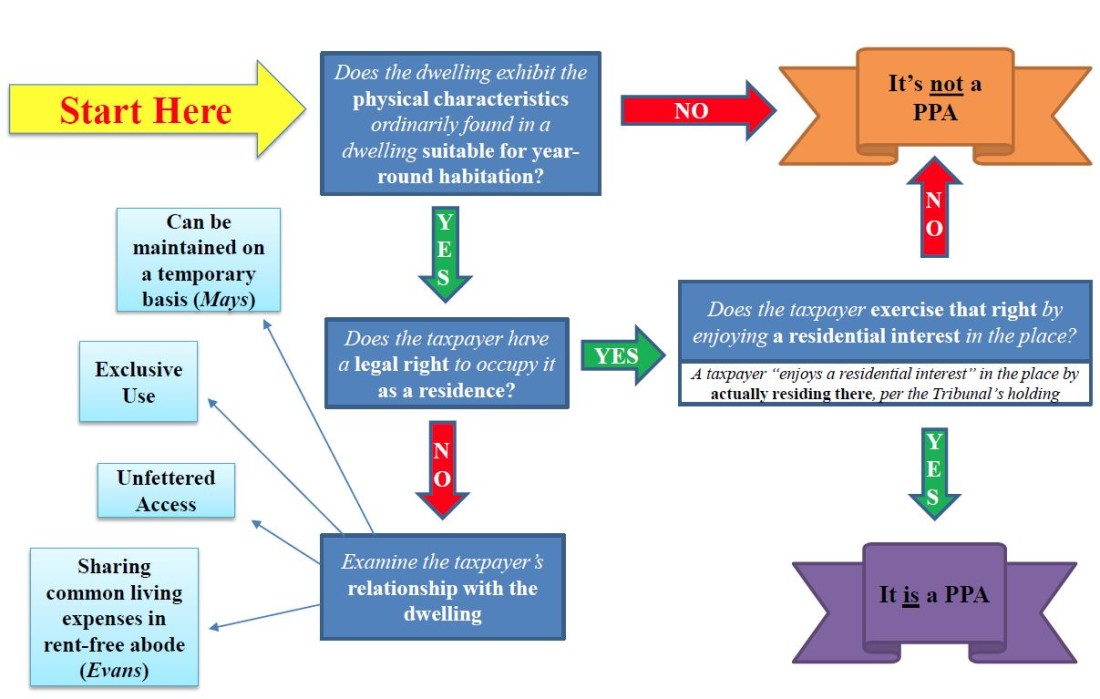

The reason the Tribunal’s analysis is so interesting is because, by walking through the various cases that have been issued over the years on the PPA test, the Tribunal ended up setting forth a very helpful framework, almost like a decision-tree, for analyzing whether a dwelling counts as a PPA for a taxpayer. Here’s what the framework looks like:

And here’s how the Tribunal explained it:

Step One. The first step in the analysis—or the “threshold question” per the Mays Tribunal—is to determine “whether the dwelling exhibits the physical characteristics ordinarily found in a dwelling suitable for year-round habitation.” If answered “no,” the dwelling is not a PPA. If answered “yes,” proceed to Step Two.

Step Two. The next inquiry is “whether the taxpayer has a legal right to occupy that dwelling as a residence.” If answered “yes,” proceed to Step Three. If answered “no,” proceed to Step Four.

Step Three. Having determined that the taxpayer has a legal right to occupy that dwelling as a residence, the inquiry is not over. Instead, under Mays the inquiry turns to whether the taxpayer “exercised that right by enjoying his or her residential interest in that dwelling.” If answered “no,” the dwelling is not a PPA. If answered “yes,” the dwelling is a PPA. And in outlining this “residential interest” step, the Tribunal pointed to Gaied, explaining in a parenthetical that “even though the taxpayer owned a dwelling, he did not use it as such, and thus it did not qualify as his residence.”

A quick side-bar here: this is really important! As outlined above, one of the most contentious issues post-Gaied was whether a taxpayer had to actually use their dwelling in order for it to be treated as a PPA. But the Tribunal seems to have resolved debate. Specifically, when answering the question as to whether Ms. Mays had a residential interest in her corporate apartment, the Tribunal looked to her actual usage of the place as a defining factor:

“Because petitioner actually resided at the [corporate apartment, which] met the physical requirements of permanency, we conclude that petitioner also enjoyed a residential interest in the apartment at the Marc for the course of her stay there.”

In any case, back to the framework.

Step Four. We arrive at Step Four only if Step Two was answered “no.” Here, having determined that the taxpayer lacked a legal right to occupy that dwelling as a residence, under Mays “the analysis turns to factors indicating the taxpayer’s relationship to the place.” This inquiry considers a variety of factors, such as whether the taxpayer has “unfettered access” to the dwelling, and whether the taxpayer is maintaining the dwelling by “doing whatever is necessary to continue one’s living arrangements” in the dwelling. This would need to be determined on a case-by-case basis.

Interestingly, the Tax Department has its own chart in their audit guidelines that they instruct auditors to use when evaluating whether a dwelling constitutes a PPA. That’s on page 99 of the guidelines, accessible in the link above. But we like this one better! It seems to provide a more helpful step-by-step guide for making the call on whether a place is treated a PPA.