SEC Adopts Final Pay Versus Performance Rules

The SEC recently adopted final pay versus performance disclosure rules, implementing Section 14(i) of the Securities Exchange Act of 1934. As added by Section 953(a) of the Dodd-Frank Act, Section 14(i) mandated that the SEC adopt rules requiring reporting companies to disclose information showing the relationship between executive compensation and financial performance. These rules apply to all SEC-reporting companies (including smaller reporting companies), except foreign private issuers, registered investment companies (other than business development companies), and emerging growth companies.

Item 402 of Regulation S-K already provides detailed disclosure rules for executive compensation and many companies have already attempted to explain in the Compensation Discussion and Analysis (“CD&A”) section of their proxy statements how executive pay is linked with company performance. However, there is no single place where companies are required to provide investors with direct comparisons of executive pay with performance. New Item 402(v) of Regulation S-K will require companies, as part of their annual proxy statements, to provide tabular disclosure regarding executive compensation and financial performance for the five most recently completed fiscal years, as well as narrative disclosure regarding the relationship between executive compensation and financial performance.

These new pay versus performance rules will be effective for the upcoming 2023 proxy season, with these new disclosures required in proxy statements relating to fiscal years ending on or after December 16, 2022. As a result, calendar year filers will need to begin preparing for these new disclosures now.

Tabular Disclosure

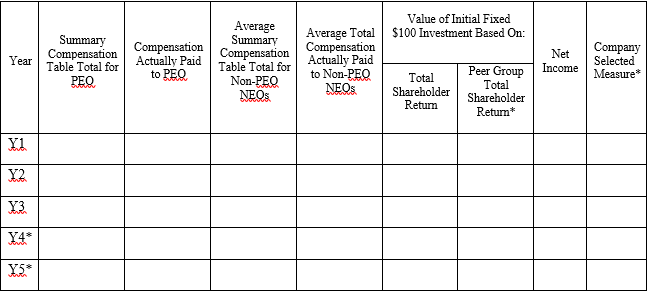

The pay versus performance table is required to disclose the following information for the last five fiscal years (or three fiscal years in the case of smaller reporting companies):

- The total compensation earned (as reported in the summary compensation table) by and total compensation actually paid to the principal executive officer (“PEO”). For this purpose, the total compensation actually paid generally represents the total compensation shown in the summary compensation table, with certain adjustments for defined benefit pension plans, stock awards, and options awards, which adjustments must be shown by footnote to the table;

- The average total compensation earned (as reported in the summary compensation table) by and the average total compensation actually paid to the other named executive officers (“NEOs”);

- The company’s cumulative total shareholder return (“TSR”) for the measurement period;

- The cumulative TSR for the company’s peer group for the measurement period. For this purpose, the company’s peer group should either be the peer group described in the company’s CD&A or the peer group used in the company’s Form 10-K performance graph disclosure;

- The company’s net income for each fiscal year, calculated in accordance with U.S. GAAP; and

- A “Company-Selected Measure” (which may be a non-GAAP financial measure) representing the most important financial performance measure (other than a measure already disclosed in the table) that is used to link compensation actually paid to the NEOs with the company’s performance.

An example of the pay versus performance table is set forth below. Asterisked items denote portions of the rules that do not apply to smaller reporting companies.

Narrative Disclosure

In addition to the tabular disclosure, companies will be required to provide a clear description of the following:

- The relationship between the compensation actually paid to the NEOs and the company’s cumulative TSR, the company’s net income and the company-selected measure for the last five fiscal years;

- A comparison of the company’s cumulative TSR and the cumulative TSR for the company’s peer group for the last five fiscal years.

Most Important Financial Performance Measures

Companies (other than smaller reporting companies) will be required to provide a tabular list of at least three, and up to seven, financial performance measures used to link compensation actually paid to NEOs for the most recently completed fiscal year to company performance. The rules do not require any additional explanation of the measures included as part of a company’s list.

Location of Disclosure

The rule provides a company with flexibility to determine where in the proxy statement that the required pay versus performance disclosure appears. In adopting the final rule, the SEC noted that mandating companies to include disclosure in the CD&A may cause confusion by suggesting that the company considered the pay versus performance relationship in making compensation decisions, which may or may not be the case. As a result, many companies may decide to include the pay versus performance disclosure outside of the CD&A.

Transition Rule

Under a transition rule, companies may initially provide disclosure for three years, instead of five years, as part of the first proxy statement that includes the new disclosures, and then provide disclosure for an additional year in each of the two subsequent proxy statements (resulting in a full five years of disclosure first being provided in the third proxy statement that is filed after the rules come into effect).

XBRL

The new pay versus performance disclosures will need to be separately tagged using Inline XBRL, subject to a phase in period provided for smaller reporting companies only. Companies will need to adjust internal proxy statement preparation timelines to allow for the Inline XBRL tagging to be completed, so consideration should be given to the time needed to complete this new step.

Featured

Partner

Partner Partner

Partner Co-Chair of the Firm, Partner

Co-Chair of the Firm, Partner Partner

Partner Partner

Partner Managing Partner

Managing Partner