The day many expected has finally come: Governor Cuomo has officially proposed his 2021 Budget and, as expected, it includes higher personal income tax rates for high-income taxpayers.

Here's our initial thoughts on the rate increase:

- It is styled as a “surcharge” (sounds better than a “tax”?), and applies to tax years 2021 -2023.

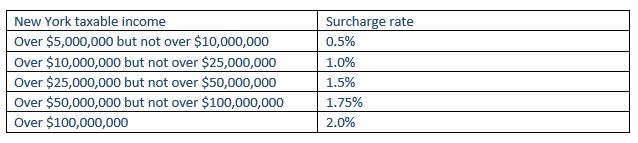

- It is based on New York taxable income, and the following bracket rates apply:

- Critically, credits don’t reduce the surcharge. So, taxpayers with huge nonrefundable investment tax credits or brownfield tax credits or movie production credits will still need to pay the surcharge and carry over the unused credits to subsequent years. We assume that refundable credits will be allowed to offset the surcharge, and hope that the final legislation clarifies this.

- The 2021 surcharge is due when the 2021 return is filed. Estimated tax penalty relief is provided for the estimated payments due April 15 and June 15, though this seems an odd provision given the explicit language that the surcharge is not required to be paid until the taxpayer files their 2021 return.

- For nonresident taxpayers with some New York source income, we believe that their surcharge rate will be based on their TOTAL New York taxable income, not just their New York sourced income. So a taxpayer with $50 million of total income but only $1 million of New York source income will still pay a 1.75% surcharge.

So overall, there’s nothing too elaborate here. It’s really just a higher tax-rate applicable to taxpayers with incomes over $5 million. And for the really high-net worth taxpayers, it amounts to an extra $2M per year in New York taxes on every $100M of income.

But, here’s the twist, and it’s a little complicated:

Taxpayers who pre-pay estimates of the 2022 and 2023 in 2021 can double-dip in 2024 and later years…assuming the law doesn’t change. The amounts pre-paid will be applied to the surcharges owed in 2022 and 2023. The double-dip is that the pre-payments also form the basis for deductions available in 2024 and subsequent years that, in effect, allow pre-paying taxpayers to apply the amounts again against the regular taxes imposed in those years. In 2024 the mechanism to permit the double-dip is in the form of a deduction equal to the lesser of: (i) the taxpayer’s unearned income (interest, dividends and capital gains) taxable in the state; or (ii) 50% of the “prepayment income equivalent.” This prepayment income equivalent (let’s call it the “PIE”) is equal to the amount of the pre-paid surcharge divided by the regular income tax rate of 0.0882. This is simply a way of converting the pre-paid surcharge from a credit to a deduction. So, for example, a $1 million pre-payment translates into a PIE of $11,337,868.48 and a possible deduction in 2024 (at 50%) of $5,668,934.24. And assuming regular State income tax rates of 8.82%, this deduction results in around $464,000 of tax savings…meaning the taxpayer could get about half of the pre-paid surcharge back in 2024.

Any PIE remaining unused in 2024 gets carried forward to future years (subject to the same unearned income taxable in New York limit but NOT the 50% limit) until the pre-payment is fully absorbed. Or, if a pre-payer dies, their estate can apply any un-absorbed (i.e. through the PIE function) pre-payments as a refundable credit on their final return.

Big picture: the pre-payers get their pre-payments returned to them as credits against surcharges in 2022 and 2023, and then again in the form of grossed-up deductions against the regular tax applied against them in 2024 and subsequent years. Any unused prepayment is carried over to the years subsequent to 2024 and may be used (through the PIE mechanism) to offset income and therefore New York taxes in those subsequent years. In short, if the taxpayer takes the 2022-23 pre-payment, they’ll eventually get the benefit of those pre-payments paid back to them. Thus, ignoring the time value of money prepaid, the impact of these new surcharges will only cause them higher New York taxes in 2021.

But there may be a catch: It is unclear how the unearned income limit will be applied to nonresident pre-payers. If a taxpayer pre-pays the surcharges and then moves out of state in 2024, their benefit could be significantly diluted, since none of their unearned income is treated as New York source income, and therefore could be viewed as not really “taxable in the state”. And since the 2024 deduction is equal to the lesser of the taxpayer’s unearned income taxable in the state or 50% of the PIE, basically this means the newly-minted nonresident could lose most of the benefit of prepayment.

So the lesson is: don’t do the pre-payment thing if you are going to move out of New York in 2024! Or at least wait until further guidance becomes available. Otherwise, this pre-payment thing seems to be a good deal for high-earning New Yorkers who decided to stay in New York (both of them, haha). But do we really trust that the Legislature in 2024 won’t change this? That presumably would raise some problems about retroactive law changes, but it nonetheless is something to keep in mind for taxpayers who are thinking about pre-paying the surcharge.

If you’d a like a look at the actual bill and the memorandum in support, you can find it here. We won’t know if this becomes law until late March or early April, when (hopefully) the final Budget is supposed to be passed. So stay tuned until then!